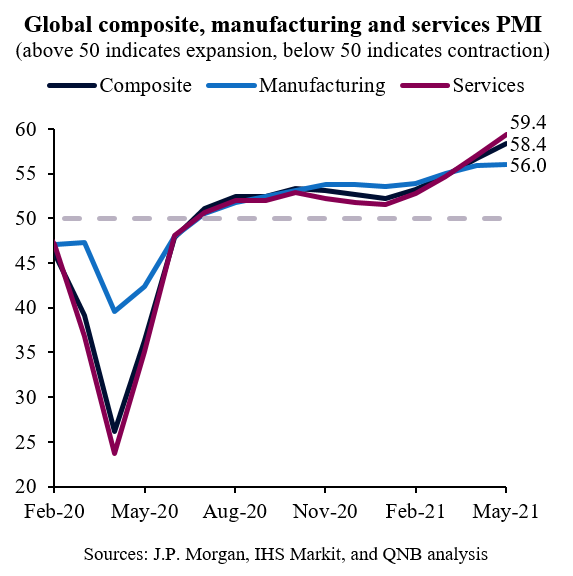

The Purchasing Managers Index (PMI) is a good and timely indicator of the global economic recovery. The PMI is a focused survey of businesses and is published within just a few weeks of the data being gathered. Whereas, GDP is a much broader measure of economic activity, which is often published months later. Fortunately, the global composite PMI is a good indicator of global GDP growth, so it is reassuring that it rose further to 58.4 in May, its highest level for over 15 years.

However, this global composite picture masks important differences between the manufacturing and services sectors. This week we unpack the global composite PMI by comparing the recovery in these two sectors in the US and Euro area.

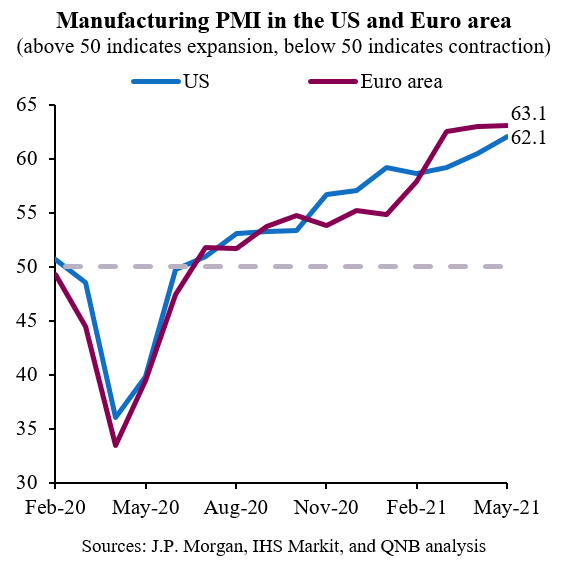

There has clearly been a strengthening recovery in the manufacturing sector in both the US and Euro area. This has been driven by two factors. First, supply recovered rapidly from the acute phase of the pandemic in April 2020. Factories, freight transportation and logistics were relatively easily able to implement effective social distancing, enabling a quick return to close to full capacity. Second, lockdowns and stay-at-home measures stimulated a temporary surge in demand for consumer goods and electronic equipment, which helped make living and working-from-home more pleasant and effective. Activities such as home delivery services, cooking at home, home-movies, video games, and video conferencing have all stimulated demand for electronics and home appliances. Further, concerns about spreading the virus discouraged people from using mass transport, in favour of travelling in private vehicles, which stimulated demand for new cars, used cars and automotive components.

The strength of the recovery in the manufacturing sector has supported economic activity throughout the second half of last year and the first half of 2021. Indeed, the surge in demand has been so strong that supply chains, freight transportation and production of key components became constrained. For example, production of older computer chips used in cars cannot keep up with demand. Firms would normally respond to stronger demand by increasing supply capacity, but much of the surge in consumer demand for goods is expected to soften as social distancing measures are eased further. They have therefore held back on some investments. We expect activity in the manufacturing to continue to expand, but at a slower pace, which implies the manufacturing PMIs will ease back closer to, but remain above, 50.

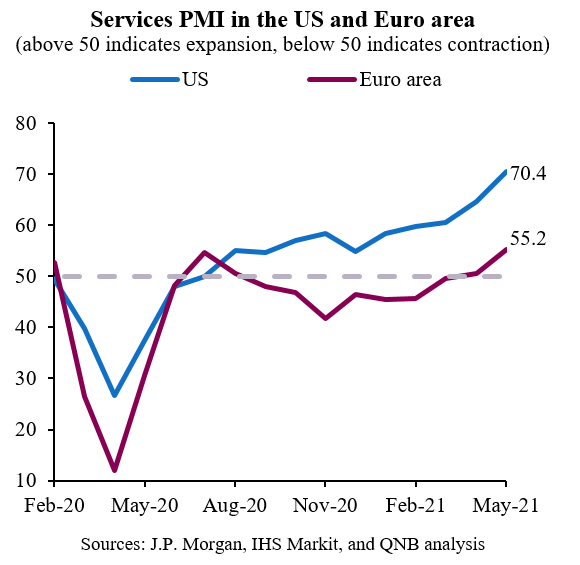

In contrast, we expect the services sector to drive the next phase of the recovery as an ever greater proportion of the population in the US and, after a slower start, the Euro area are vaccinated. We see three key drivers. First, vaccinated people are less likely to spread the virus and much less likely to become seriously ill from it. Indeed the number of new infections and hospitalizations are now at a low enough level for the US and Euro area countries to continue to ease social distancing measures, allowing the reopening of their economies. Second, the return of warmer weather will make it easier for people in the US and Euro area to spend time outside where the virus spreads much less easily. Third, after so much time at home there is pent-up demand to spend more time and money on domestic services, such as eating out in restaurants, outdoor activities and entertainment. The strength of the recovery in the US is clear with the services sector PMI increasing to over 70. Whilst the beginning of the recovery is observable in the Euro area with the services sector PMI rising above 55 in May.

We expect the shift in consumer demand from manufactured goods to domestic services to drive the next phase of the recovery in the US and Euro area.

Download the PDF version of this weekly commentary in English or عربي