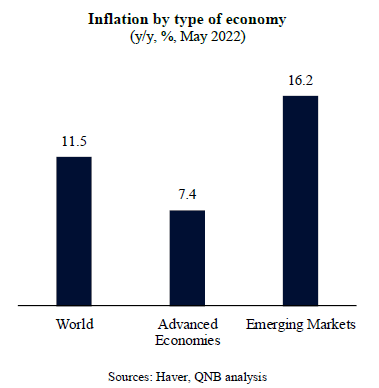

High and rising inflation has dominated the economic agenda in recent months. The combination of robust policy-induced global demand growth with pandemic-related supply constraints led to a significant uptick in consumer prices. While most of the discussions about inflation tend to be concentrated on the challenges that it poses to the US and European economies, emerging markets (EM) are also affected. In fact, EM inflation is well within the double digit space, significantly higher than its 10-year average of 5.2% or the current 7.4% figure for advanced economies.

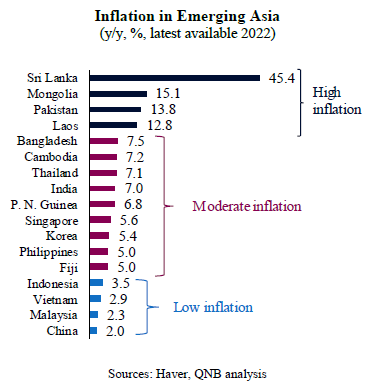

However, not all of the EM are in the same position when it comes to inflation. In emerging Asia, for example, there is a wide range of inflation prints running from low inflation to very high chronic inflation. In this piece, we differentiate between high, moderate and low inflation. High inflation is defined here as a year-on-year (y/y) consumer price increase that is at least 200 basis points (bps) higher than the 6.5% long-term inflation average for the region. Moderate inflation ranges 200 bps around this average, i.e., it ranges between 4.5% and 8.5%. Low inflation includes rates that are below 4.5%.

Our analysis dives into the reasons behind such divergence in inflation figures across emerging Asia. In our view, one main factor dominates the overall price dynamics of each bracket of countries we analyse. This one dominating factor however is different for each bracket. We have identified income level as the dominant driver for high inflation countries, imported inflation for moderate inflation countries and improvements in current account positions for low inflation countries.

All emerging Asian economies that currently face high inflation are low income countries, i.e., countries that present a GDP per capita around or below USD 12 thousand. This includes Sri Lanka, Mongolia, Pakistan and Laos. According to the International Monetary Fund (IMF), USD 12 thousand is the average income per capita in developing and emerging Asia. In those countries, high inflation is explained by two factors, both associated with low income conditions. First, their average consumer basket tends to have a high weight of essential goods, such as food and energy. This means that food and energy absorb a higher amount of income relative to the total income available. Unfortunately, due to different global supply shocks coming from the pandemic and the Russo-Ukrainian conflict, food and energy are the products under more price pressures across continents. As a result, lower income countries are more likely to experience higher inflation than countries where energy and food represent a smaller share of total consumption. Second, low income countries are negatively affected by a lack of adequate infrastructure, capital and organizational expertise. This makes it difficult for them to substitute higher cost imported goods for lower cost domestically produced goods. Thus, price pressures from external shocks become more difficult to absorb, as local production rarely provides cheaper domestic alternatives to expensive imported goods in an effective manner.

The majority of emerging Asia is experiencing moderate inflation. This includes Bangladesh, Cambodia, Thailand, India, Papua New Guinea, Singapore, Korea, Philippines and Fiji. In their case, inflation rates are still significantly below global inflation and even below inflation in major advanced economies, where it is currently running around 7%. Importantly, all these countries are net energy and commodity importers, which makes them particularly vulnerable to the recent rise in oil and agricultural prices. This suggests that a large share of the current rise in prices is due to imported inflation. This has been amplified by the ongoing depreciation of their currencies, partially driven by the negative shock on their current accounts.

A few emerging Asian countries are running against the global trend, presenting low inflation figures. This includes Indonesia, Vietnam, Malaysia and China. They are all benefiting from improvements in their current account balances. The drivers for this, however, are different. In Indonesia and Malaysia, they are associated with commodity prices. As net commodity exporters, they both benefit from higher fiscal and external revenues. While fiscal windfalls support the funding of food and energy subsidies, external windfalls protect the local currencies against global headwinds, preventing inflationary depreciations and devaluations. In China and Vietnam, booming exports and subdued domestic consumption are also favouring an improvement in their respective current account positions. This supports their currencies while allowing for the continuity of a growth model that tends to be deflationary, i.e., that combines relatively low domestic consumption with excess savings that are allocated into new investments. In China, this was further supported by the slowdown caused by social distancing measures imposed during the most recent Covid-19 outbreaks in the country.

All in all, inflation figures reflect different patterns in emerging Asia with varying root causes. Low income countries face high inflation because of the composition of their consumption basket and their inability to substitute higher cost imports. Net commodity importers face moderate inflation because of high commodity prices and inflationary currency depreciations. Countries with an improving current account position face low inflation because of the resilience of their currencies, their capacity to maintain subsidies and moderate domestic demand.

Download the PDF version of this weekly commentary in English or عربي