The United Kingdom (UK) has long held a reputation for sound policymaking, but the last few months have been a roller-coaster ride by comparison. Indeed, Liz Truss set a new record as the UK’s shortest serving prime minster (PM) when she resigned after only 44 days in office. Her prime policy mistake was a so-called “mini budget” which was rushed through and side-stepped the usual scrutiny by the UK’s Office for Budget Responsibility (OBR).

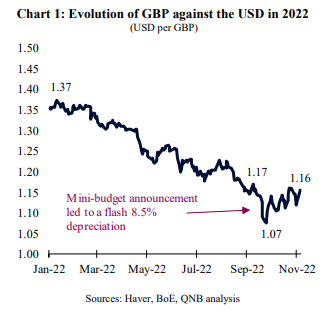

In terms of policymaking, Truss’ budget was anything but “mini” as it attempted massive policy changes and most importantly implied wider fiscal deficits due to unfunded tax cuts. Financial markets reacted aggressively with the GBP depreciating sharply (Chart 1) and the yields on UK government debt (gilts) spiking higher. Indeed, the Bank of England (BoE) was forced to intervene to protect pension funds from bankruptcy as they had taken leveraged bets on gilt yields remaining low.

As a result, Liz Truss stepped down and Rishi Sunak took over as PM on 25th October 2022, taking the reins of a country facing four significant economic headwinds: tightening fiscal policy, tightening monetary policy, an evolving European energy crisis as well as Brexit induced labour shortages.

First, PM Sunak, himself a former chancellor of the exchequer (UK finance minister) has already announced a significant tightening of fiscal policy, effectively reversing all of Truss’s policy changes. Sunak and his chancellor, Jeremy Hunt, are looking for a combined GBP 50 billion in tax increases and spending cuts to balance the books. Whatever details this may contain, the new budget must include a significant tightening of fiscal policy in order to rebuilt the UK’s reputation. However, this will unavoidably act as a significant headwind to the outlook for the UK’s GDP growth.

Second, the highest inflation in over 30 years (around 10% in September) and the weakness of GDP are forcing the BoE to increase interest rates aggressively. The 75 basis point (bp) hike in November is likely to be followed by further 50 bp hikes in both December and February, leading to a peak policy rate of over 4% in 2023. This aggressive tightening of monetary policy will coincide with the similar tightening in fiscal policy noted above. Therefore, tightening monetary policy will also be a significant headwind for the UK outlook, with fiscal and monetary policy re-enforcing, rather than offsetting, each other.

Third, record high European gas prices are pushing up on costs for producers, prices for consumers and government spending through support measures, such as cross subsidies and price caps. Leaving the European Union (EU) has gifted the UK greater policy flexibility, which has allowed it to be more proactive in reacting to the crisis, including via faster implementation of support measures to households and corporates than EU countries. Nevertheless, higher energy prices and the drain on government finances are both inevitably still acting as headwinds to the economic outlook.

Fourth, the supply side of the UK economy is constrained by labour shortages that are a legacy of the UK’s decision to leave the EU. The UK’s agriculture, manufacturing and services sectors had all become accustomed to the plentiful, low cost labour that was available from countries in Central and Eastern Europe. However, that changed with Brexit excluding the UK from the EU’s policy of free movement of labour. The global Covid-19 pandemic further exacerbated the situation and the UK is now left with severe labour shortages across many sectors of the economy. That, in-turn, is causing persistent upward pressure on wages and therefore also inflation, despite the weakening outlook for demand. Therefore, labour shortages present another headwind for the UK economic outlook.

All in all, PM Sunak is taking the helm of a country that is currently exposed to several economic uncertainties that will continue to simultaneously disrupt supply and demand. On the one hand, UK consumers will face lower disposable income. On the other hand, UK producers are exposed to higher costs and lower competitiveness, which affects their overall profitability. All in all, this will be negative for both consumption and investment, capping UK growth in the short- to medium-term.

Download the PDF version of this weekly commentary in English or عربي