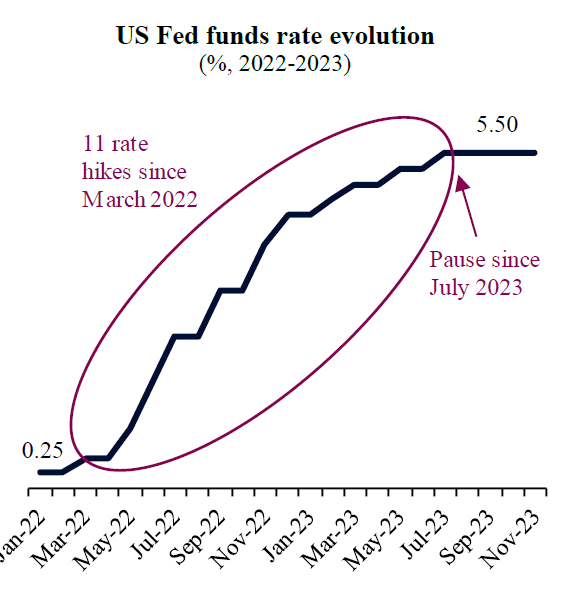

The US Federal Reserve (Fed) has kept its benchmark policy rate unchanged at its November and September 2023 Federal Open Market Committee meetings. These decisions marked a significant “pause” of the tightening cycle that started in March last year, after eleven rate hikes pushed the Fed funds policy rate to the highest levels in more than 20 years at 5.25-5.5%.

In February 2023, markets were pricing additional rate hikes that would be kept for longer. However, the US regional banking crisis in March, following the deposit run on California-based Silicon Valley Bank, led to renewed bets of an early Fed pivot with significant policy rate cuts. These concerns were later tempered by the rapid stabilization of US banks and a remarkable economic re-acceleration, driven by robust consumption and strong labour markets. Such positive trends gained further momentum over the summer, as US GDP printed an extraordinary growth of 4.9% annualized in Q3. As a result, bets for higher rates for longer resurfaced.

There is still an unfinished debate about whether the Fed is ready to wind down, “pause for longer” or even pivot the policy rate changes sooner rather than later.

In our view, under current conditions, the Fed is likely to maintain existing policy rates at elevated levels at least until late Q2 2024.

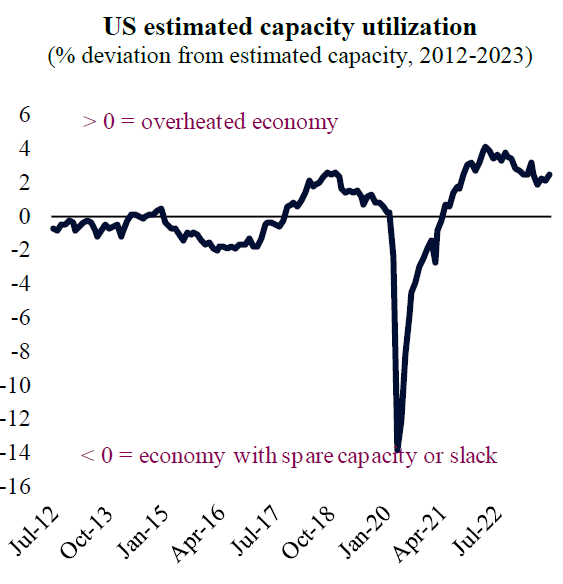

On the one hand, there is little room for an early pivot for rate cuts before Q2 2024, as the US economy remains overheated. US capacity utilization, measured taking into account the state of the labour market as well as industrial spare capacity, suggests that capacity constraints still exist. In other words, there is currently higher demand for labour than employees available, whereas industrial activity is running above its long-term trend. These conditions may lead to rapid price increases should commodity prices surge or domestic consumption re-accelerate. The Fed is unlikely to cut rates until the labour market weakens more and industrial spare capacity increases. This would serve as a buffer for the economy to absorb shocks without the risk of rapid inflation outbursts should the targeted economic slowdown not appear as scheduled.

US estimated capacity utilization

On the other hand, interest rates have not only “normalized” but are significantly restrictive. This means that rates are above both the running inflation rate (3.7%) of what is considered the “neutral” level for interest rates (4.2%), i.e., the rate where it neither supports nor drags spending, investment and economic activity. Hence, over time, high nominal and real rates are set to weigh on GDP, leading to further downward adjustments in aggregate demand and economic activity. In other words, the Fed does not need to “catch up” anymore by hiking rates to combat inflation. As time should work in its favour, the measures taken by the Fed which have typically a six months lag effect would start to “kick in”. This would lead to a reduction in consumption and investments for households and corporates. Consequently, labour markets would adjust, industrial demand weaken, taking inflation in the direction the Fed wants.

All in all, we are rather expecting a long “pause” until new data presents a clearer path for policymaking. Capacity utilization is still too tight, favouring wage growth rates that are inconsistent with below target inflation. Nevertheless, restrictive interest rates should gradually work in favour of lower activity and inflation reduction over time, even if it could lead to a sharper downturn or recession in 2024.

Download the PDF version of this weekly commentary in English or عربي