A lot has been written in recent months about whether the US, Euro area and global economies are heading for a recession. It is clear that the global economy is facing several material headwinds and experiencing a sharp slowdown in 2022. It is less clear whether we will actually see a global recession.

This week, we define and assess the risk of recession in the US, Euro area and global economy before concluding what this could mean for the economic outlook.

The accepted definition of a recession is two consecutive quarters of negative GDP growth. However, global GDP growth is so robust that this condition is rarely met and many analysts loosely refer to a sharp slowdown as a recession.

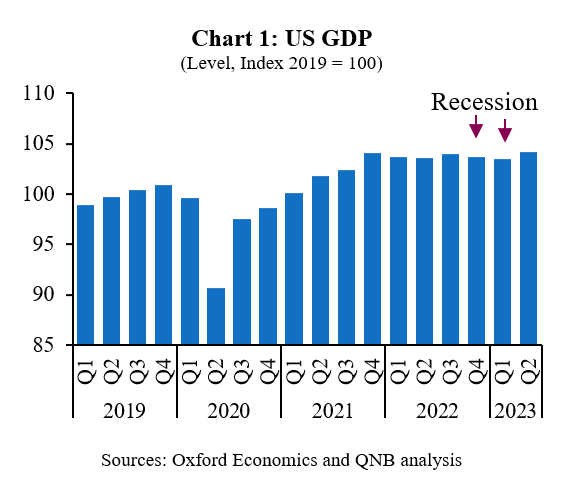

First, we consider the US economy, which is slowing rapidly and makes the idea that the Federal Reserve (Fed) can engineer a soft landing optimistic, at best. Leading indicators, derived from PMI surveys, equity markets and US Treasury markets, are all pointing to a deterioration of US macro conditions. Indeed, slower inventory accumulation has already led to two quarters of contraction in US GDP in Q1 and Q2 2022. While this could be interpreted as a technical recession, the US Bureau of Economic Analysis (BEA) may decide to not consider it an official recession, as consumption and other key metrics are still strong. Perhaps more importantly, the Fed has become increasingly aggressive with its policy tightening as high inflation has proven to be more persistent than previously expected. Higher interest rates will act to further dampen the US economic outlook and we now see a mild recession, with small falls in GDP likely in both Q4 2022 and Q1 2023 (Chart 1).

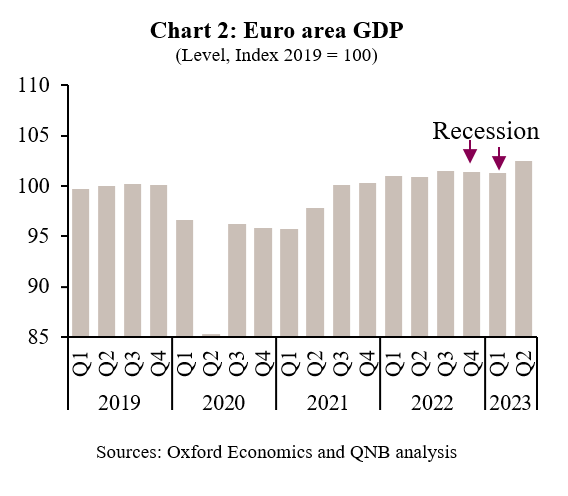

Second, we consider the Euro area, which is seeing a divergence between manufacturing and services. On the one hand, industrial production is plagued by supply-chain bottlenecks, higher input costs, and weakening sentiment. On the other hand, the services sector is still benefiting from experiencing a post-pandemic reopening rebound. However, on top of this, we have Europe’s dependence on Russian energy, which is being heavily restricted by the war in Ukraine and pushing European energy prices to unsustainable highs. Even if the situation doesn’t get worse, then the existing headwind from high energy prices is expected to push the Euro area into recession, with small falls in GDP likely in both in Q4 2022 and Q1 2023 (Chart 2).

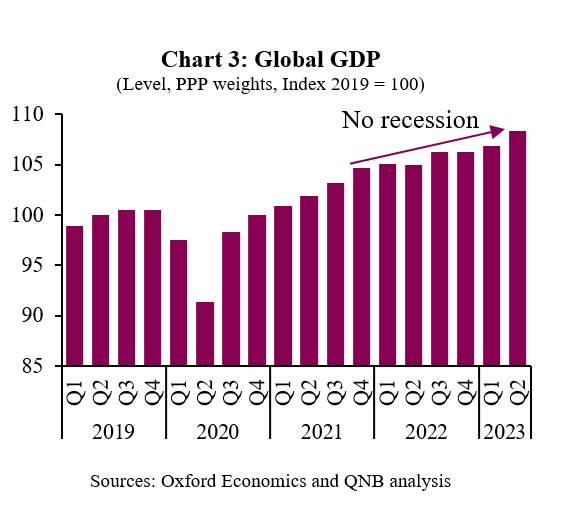

Third, we consider the economic outlook for the Rest of the World (RoW). The main driver of global GDP growth is the continued re-opening of economies as high levels of vaccination help to minimise the residual impact of the pandemic in most countries. China is an exception, but policy stimulus is expected to drive a modest recovery with further growth and no recessionary risks, despite China’s Covid-Zero strategy acting as a persistent headwind.

Taken together, continued growth in China and the RoW is expected to be sufficient to avoid a global recession, despite the likelihood of recessions in the US and Euro area (Chart 3). This outlook assumes that energy prices do not rise significantly higher and that interest rates hikes by major central banks do not cause a financial crisis with a hard landing. Interestingly, the forecast for global GDP growth of around 3% in 2022 is only a little weaker than the compound average growth rate of 3.4% since 1992.

Download the PDF version of this weekly commentary in English or عربي